Who Regulates Banks in Georgia? A Practical Guide to the National Bank and the Financial Regulations Landscape

- Jun 22, 2025

- 8 min read

Table of contents

Why You Should Care About Banking Rules in Georgia

Opening a business account in Georgia is fast. But staying compliant? That’s where founders get tripped up.

Whether you're setting up a startup, moving your HQ, or managing payments from abroad, you’re operating inside a financial system that runs on rules. The good news? The rules are public, stable, and mostly business-friendly.

But if you ignore them, by accident or assumption, you risk delayed accounts, frozen transfers, or worse, flagged activity that scares off your clients or partners.

Understanding how bank regulations in Georgia work helps you choose the right bank, stay in good standing, and avoid unnecessary stress. This is especially true if you're not on the ground and are relying on a team, a lawyer, or remote setup services.

Who's Actually in Charge?

The National Bank of Georgia.

It’s the country’s central bank and regulatory authority. Think of it as the financial traffic controller. It decides which institutions get a license to operate and makes sure they follow the rules.

Its job is to:

Keep the financial system stable

Manage monetary policy and inflation

Supervise commercial banks and microfinance organizations

Enforce anti-money laundering (AML) standards

It doesn’t report to any commercial bank. It doesn’t answer to politicians. It works independently, which is part of the reason Georgia’s economy has attracted so much international trust.

If you're opening an account with Bank of Georgia or TBC Bank, you're operating in a system they don’t control. The National Bank calls the shots.

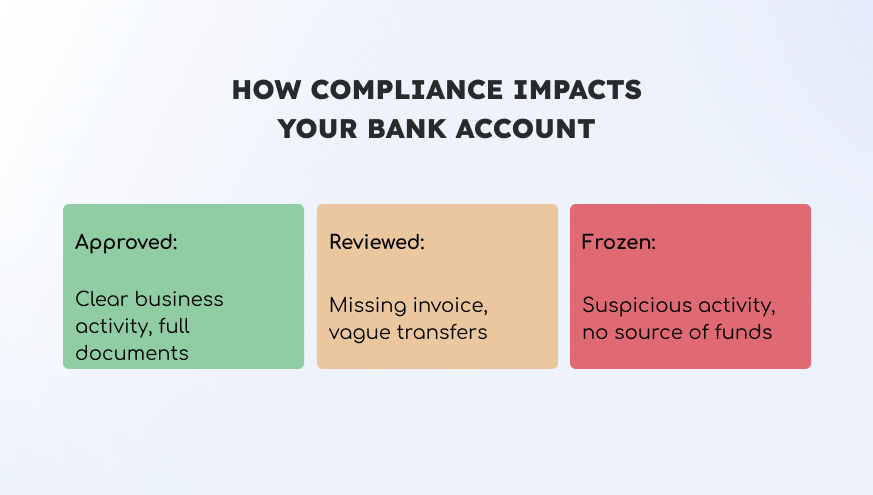

What This Means for Your Bank Account

When a bank approves your application, it’s not just about customer service or liking your passport photo.

It’s about risk.

Each bank is required to check your documents, verify your business activity, understand where your money is coming from, and report anything suspicious to the National Bank.

So if:

Your company was just registered

Your business activity is vague

You’re receiving high-value international payments with no invoices

Then your account is more likely to get flagged, delayed, or frozen.

This is why banking compliance matters. And why it’s not just about choosing a bank, it’s about preparing for how that bank thinks.

Want to stay out of trouble? Read this first:Banking Compliance in Georgia: Avoiding Common Mistakes and Penalties

What Makes a Bank Legit in Georgia?

Every licensed commercial bank in Georgia has gone through a strict approval process.

To even get licensed, a bank must:

Prove its business model and capital reserves

Show internal risk systems and KYC processes

Pass financial and operational reviews by the National Bank

Once they’re up and running, they’re not off the hook. Licensed banks are monitored constantly. They file reports. Submit financial statements. Undergo compliance checks. Respond to supervisory audits.

And if a bank fails to follow these rules? The National Bank can suspend, fine, or revoke their license.

This is why Georgia’s biggest banks, like Bank of Georgia and TBC Bank Georgia, put so much emphasis on documentation. Not because they’re being difficult, but because their own license depends on it.

Financial Rules That Affect You Directly

Georgia isn’t overly regulated. But it is properly regulated.

Here are a few policies that affect your account:

AML and KYC checks

Every payment that looks “off” may be reviewed. Banks need to know where the money comes from. If it doesn’t match your declared activity or you don’t respond to a query, they can freeze your account.

No strict capital controls, but...

You can move money in and out of Georgia fairly easily. But large transactions, especially from abroad, might need supporting documents, like contracts or invoices.

Bank secrecy exists, but isn’t absolute

Your data is protected. But banks must cooperate with tax and legal investigations. So don’t assume your activity is invisible.

Non-residents are watched more closely

If you’re not a Georgian resident, the banks will usually request additional documentation. Sometimes this includes proof of business activity in or outside Georgia.

Need to know what exact documents you'll need? Here’s the full checklist

How Foreigners Fit into Georgia’s Banking Landscape

For non-residents and international founders, the rules don’t change but scrutiny is higher. The National Bank of Georgia requires banks to take extra care when dealing with foreign identification, remote addresses, and international transfers.

Extra KYC checks on non-residents

If you live outside Georgia, the bank will ask for notarized copies of your ID, proof of local or international address, and explanation of your economic ties. Some branches may also require a face-to-face meeting or verification via video call. It’s standard compliance, not discrimination.

Source of funds becomes crucial

Banks need to know your money’s origin. International clients or investors require contracts, invoices, or agreement letters. Without explanations, transfers may be held or refused, even if the amounts seem routine.

Beneficial owner reporting

Georgian banks must report complex ownership structures to the National Bank. If you're a minority shareholder, nominate someone local or consider a nominee director. This helps clarify your ownership for compliance purposes.

Remote access often takes time

Activating international transfer rights or installing secure tokens may require branch visits. Even with a digital-native process, banks may delay approvals as part of risk monitoring. It's slow by design.

What Banking Regulations Are Coming in 2025 and Beyond

Georgia’s financial system is evolving quickly, and the National Bank is updating rules to keep pace.

Fintech and digital payment regulations

New payment institutions must register and follow AML/KYC procedures. Some foreign fintech apps will welcome Georgian clients, while others might get blocked due to lack of local licensing.

Crypto-adjacent regulations

Cryptocurrency remains unregulated in Georgia but banks will view crypto-linked transfers with extra caution. Expect higher compliance thresholds if you receive crypto proceeds.

Tightening tax collaboration

International tax cooperation is expanding. Banks must share account information with global bodies. If you're billing clients in multiple countries, make sure your company is transparent about tax residency and income.

Cross-border transaction reporting

New thresholds for reporting international transfers may be added, especially from non-OECD countries. This means even routine payments might trigger compliance alerts.

Consumer protection is improving

New rules on overdraft, fair banking fees, and dispute resolution are in motion. They benefit you as a customer, but they also mean stricter checks when your banking behavior falls outside the norm.

Staying Compliant: Best Practices for Businesses

Regulations only matter when they affect your operations. Here's how to stay ahead:

Account setup and early checks

Apply with full documentation, passport, address proof, company registration. Include bank account documents Georgia such as utility bills or office lease. A clean application speeds up the review.

Write a clear business activity description

Banks assess your risk based on field of operation. A concise one-sentence statement like "We provide SaaS services to EU clients under annual contracts" sets expectations and explains your cash flows.

Share invoices and agreements proactively

Large or repeated transfers? Provide supporting documents ahead of the transfer date. This stops compliance requests, or even freezes, before they happen.

Stay responsive to bank requests

If the bank asks for annual KYC updates or additional ID, respond within 48 hours. Slow responses increase your risk profile and may lead to account restrictions.

Treat your account as a regulated asset

When receiving payments, verify bank reference fields and transaction naming. When sending, provide full details for beneficiary identification. Even small omissions like reference codes can trigger manual reviews.

Know when to upgrade account tiers

Your bank may offer corporate-grade accounts with higher limits and dedicated relationship managers. These are designed for businesses with regular cross-border payments. Use them when your turnover or payment volume grows.

Stay tax compliant too

If your turnover exceeds 100,000 GEL a year, you must register for VAT. The bank may share data with tax authorities. Consult a tax advisor and submit returns accurately.

What Happens If Things Go Wrong

Even with precautions, you may run into compliance issues. Here’s how to bounce back:

Account freezes

Rare but real. They usually last from a few days to two weeks. To immediately resolve them:

Check your bank notifications

Address the reason (e.g. missing invoice, outdated ID)

Submit the required documents

Request a chance for formal written explanation

Denied foreign transaction

If your payment is blocked, ask your bank which compliance rule was triggered. Sometimes you need to resubmit supporting contracts or create a new transfer using more detailed fields.

Loan application declines

If your first loan request is rejected, review your financial history. Do you have clear bank statements? Contracts? If not, build a paper trail of your activities and reapply in 3–6 months.

Changing banks under NBG rules

If a bank refuses to cooperate reasonably, you can file a complaint with the National Bank of Georgia. They manage appeals and monitor banks for systemic issues.

How to Choose a Bank That Works with You

Choosing a bank is more than picking the lowest fee.

Find a bank with startup or foreigner-friendly account rules

Some banks won’t open accounts for remote founders. Others delay verification for crypto business. Ask about foreign transfer support and expected compliance turnaround times.

Match your business type with bank services

If you invoice clients abroad, go for a bank with multi-currency tools and no transfer caps. If local SMEs are your main clients, look for loan offerings and local branch access.

Look for digital-first or branch-first banks

Digital banking is fast if you already passed KYC. Branch-first banks may take longer, but they can approve IRL documents on the spot.

Choose a bank with clear escalation paths

Ask how disputes are handled and how senior management can intervene. If a compliance problem impacts your business, having fast help makes a big difference.

Stay ok with compliance services

And finally, invest in regular compliance checks. You can do it internally, or use compliance services like those from Gegidze. A small annual fee can prevent big operational delays.

Final Takeaways on Bank Regulations Georgia

Bank regulation in Georgia is transparent, consistent, and structured. The system is designed to support both local businesses and global entrepreneurs.

That means:

Predictable behavior from licensed banks

A central authority enforcing rules fairly

Progressive monitoring of compliance, AML, and financial activity

Clear pathways to resolving issues or escalating disputes

But none of this works without preparation and diligence. Whether you're a startup aiming for fast transactions or an SME seeking foreign investment, treat regulation as a tool, not an obstacle.

Need Help With Compliance or Banking Setup?

International banking is tricky, even in Georgia. If you want help picking the right bank, preparing documents, or setting up compliant systems, Gegidze can help.

We work directly with the banks, understand their internal compliance cycles, and can support remote founders or in-person clients at any stage.

Reach out today to set up your banking and compliance properly from day one.

Frequently asked questions (FAQ)

What is the National Bank of Georgia and what does it do?

The National Bank of Georgia is the central authority responsible for financial supervision, monetary policy, inflation control, and banking regulation. It issues licenses to banks, monitors their operations, and enforces compliance rules, including anti-money laundering procedures and risk controls.

Are bank regulations in Georgia strict for foreigners?

Foreigners can open accounts easily, but compliance is tighter. Banks will ask for translated documents, proof of business activity, and may require in-person visits or notarized ID copies. Non-resident clients should be ready to explain their economic ties to Georgia.

What happens if my bank account gets frozen in Georgia?

Account freezes usually occur due to missing documentation or suspicious transactions. Responding quickly with contracts, invoices, or updated ID can resolve most issues. If the bank doesn’t cooperate, complaints can be filed with the National Bank of Georgia.

How do banks in Georgia handle international payments and AML compliance?

All banks must follow strict AML regulations, including Know Your Customer (KYC) checks and transaction monitoring. For large or irregular payments, they’ll request supporting documents like contracts or invoices. Inconsistent activity can lead to account holds or compliance reviews.

How can I stay compliant with banking regulations in Georgia as a startup or SME?

Maintain clear business descriptions, keep your documentation up to date, respond quickly to bank inquiries, and organize your financial records. Using a local expert like Gegidze ensures your setup meets bank expectations from day one.